Making a new home purchase, or refinancing the one you are in now, can be a huge undertaking. This is especially true for first-time home buyers. In the midst of all the excitement of choosing a new home and making preparations, you want to get the best deal and the best mortgage rate possible.

Understanding the Components Involved in Calculating a Mortgage Payment

There are many considerations involved in calculating a mortgage for your new home purchase. Let’s take a look at several of the important terms you will need to understand.

Loan Programs

Various loan programs are available to assist would-be homeowners with making a new home purchase. The most common are backed by the federal government: FHA (Federal Housing Administration), USDA (United States Department of Agriculture), and VA (Veterans Administration).

Loan Amount

This is the amount of money you will need to borrow from a lender for your new home purchase. Subtract your down payment from the total price of the home. This is your loan amount.

Interest Rate

This is the base rate (not the APR) for your mortgage loan. This will vary depending on your location, credit rating, and other factors.

Term

This is the length of your loan, or how long it will take to pay off the loan. Longer terms have smaller payments, and shorter terms have larger payments. You will also pay more interest over a longer term.

Savings from Early Loan Payoff

This is the amount of money you can save on interest by paying off your mortgage loan early. Some loans are structured to allow for early repayment and interest savings.

Mortgage Insurance

Some lenders require you to obtain mortgage insurance if your down payment is less than 20% of the purchase price. Some government mortgage programs (like USDA and FHA) have mandatory initial and annual mortgage insurance or guarantee fee payments. This also depends on other factors about your loan with these programs.

Property Taxes

Property taxes are often included into mortgage payments for convenience. You will need to speak with your real estate professional or local loan advisor about property taxes in your area.

Homeowners Insurance

All mortgage lenders require you to carry homeowners insurance to protect their investment in your new home purchase. These payments are often also included in your monthly mortgage payment.

Calculating Your New Home Purchase Mortgage

While you may not have to be a math professor to calculate your new home purchase mortgage, it does help to have some understanding of how the calculations are performed. The basic formula used for calculating a mortgage is below:

M = P [ I(1 + I)^N ] / [ (1 + I)^N – 1]

The elements of this formula are:

- M – Monthly payment

- P – Principal (Loan balance)

- I – Interest rate (Base, not APR, divided by 12 to get your monthly rate amount)

- N – Number of payments (a 25-year mortgage has 300 payments: 25×12)

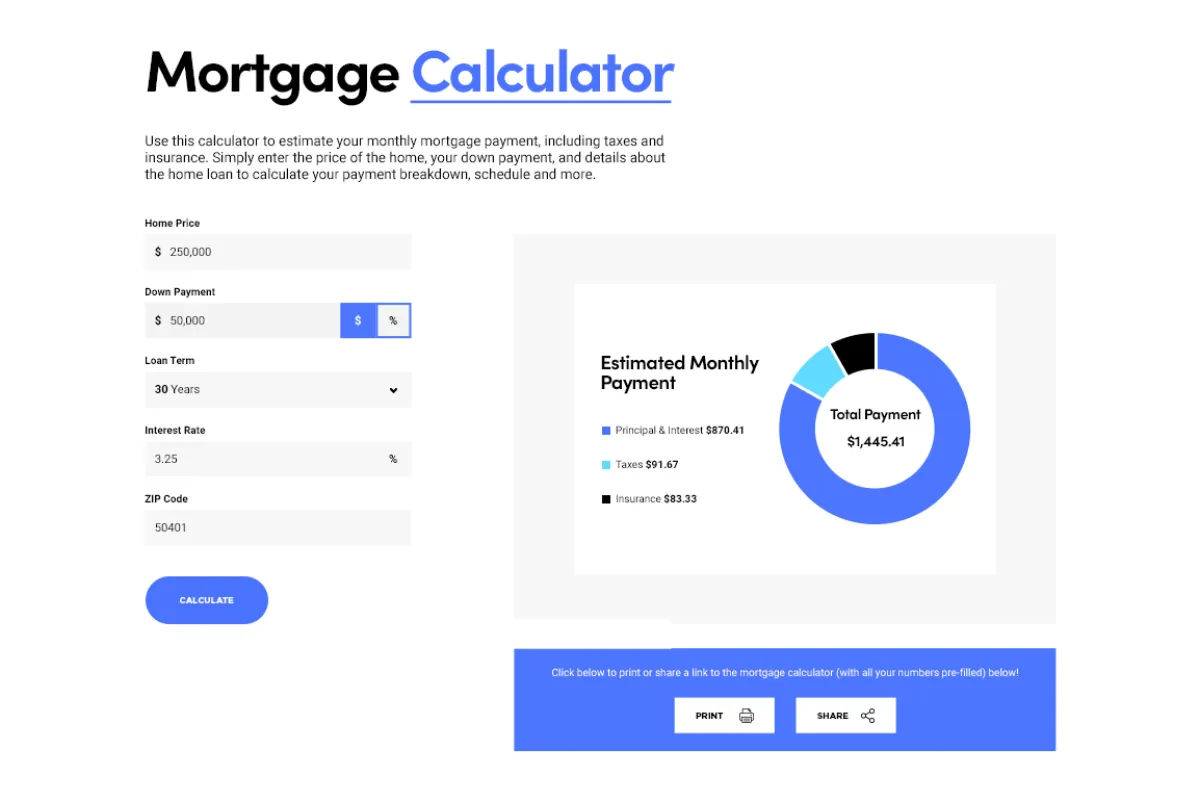

Of course, you can spare yourself lots of time and headaches by using Better Rate Mortgage’s Online Mortgage Calculator. All you need to do is enter the total price of the home, the amount of your down payment, and other details about your mortgage loan. The calculator handles the rest! There are even places to enter your property taxes, homeowners insurance payments, and HOA fees (if applicable). You can also add in any one-time expenses, such as home inspection fees.

In an instant, you can view:

- Monthly payment amount

- Total of all payments

- Detailed mortgage payment schedule

You can also access our other FREE online tools like:

- Get a Pre-Approval Letter

- Refinance Analysis Calculator

- Home Value Estimate Calculator

Contact Better Rate Mortgage today to see how easy it can be to get a mortgage for your new home purchase!